ACE Credit Restoration has over 15 years of experience in credit repair and is an innovator in the credit restoration space.

As such, we have just launched a new program, only available through ACE, that will DELETE derogatory accounts and inquiries from All 3 Credit Bureaus in 30 Days or Less and bankruptcies in 60 days or less and restore a person to Excellent Credit in that time frame, as well!

Just Some of the areas In Which our clients are benefiting With this Exclusive program:

And So Many More...

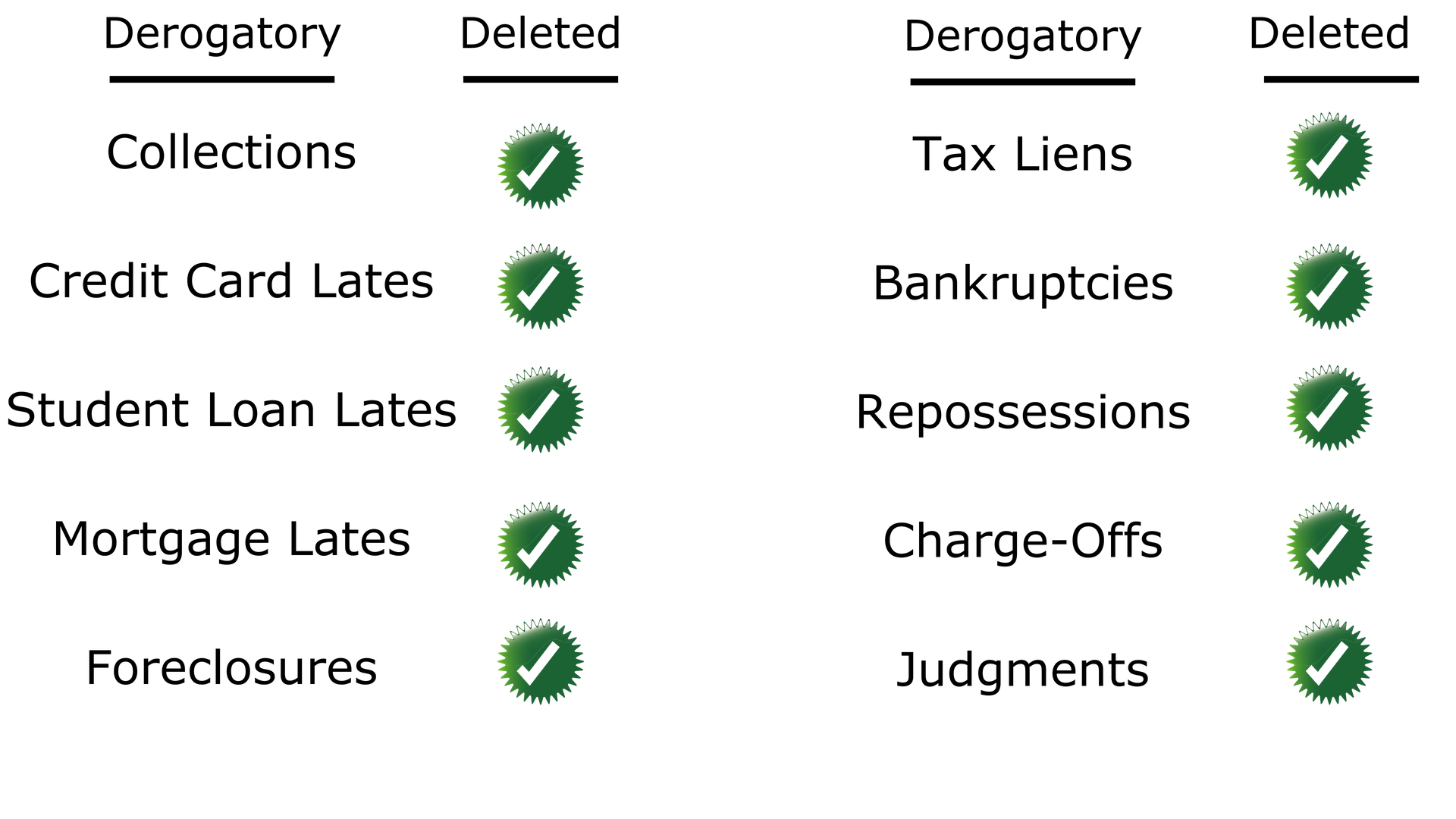

We Can Delete These Derogatory Items From Your Credit Report: